TL;DR: What are stablecoins? Originally conceived as an alternative to cryptocurrency volatility, governments and companies are discussing the use of stablecoins to fulfill many purposes. Although there’s still discussion about what they are, stablecoins can change the future of finance.

On November 10th, 2021, Bitcoin reached an all-time high of $68,789. This peak surprised traders and investors alike, but price fluctuations for Bitcoin are extremely normal. Ever since the beginning of the COVID-19 pandemic, Bitcoin’s price has fallen nearly 50 percent.

Let’s bear in mind that Bitcoin, and many other cryptocurrencies, are barely fifteen years old. Compared to gold or fiat currency, which has been around for some time, cryptocurrencies are incredibly susceptible to supply and demand, speculation, investment product hype, investor panic, and competition. While many investors are still wondering if it can reach a stable point, other experts have been looking for alternatives to solve volatility and crashes.

This is where stablecoin comes into play, and it’s not a mere understudy.

What are stablecoins? Well, there are many definitions.

Simply put, stablecoins are a type of cryptocurrency fixed to another asset, such as gold or the US dollar. They are linked to hard assets, which means the organizations issuing them must hold a reserve that allows owners to cash out the coin.

Nevertheless, Alexander Lipton, Managing Director at Bank of America and Professor of Mathematics at Imperial College London, notes that stablecoins could be “simply old wine in new bottles.” One of the main reasons for such a statement is the lack of consensus on an accepted definition. Is stablecoin a new form of money, or is it a type of existing currency with a digital twist?

Before 2008, the word “coin” referred to actual minted currency. It didn’t matter if people talked about dollars, euros, or yen; a coin was a coin. But, once Bitcoin came into the scene, the definition broadened to incorporate all cryptocurrency projects.

The earliest stablecoin projects, such as Tether or Bitfinex, tried to steer away from the volatility of digital coins using tokens backed by liquid reserves. That’s why the European Central Bank first defined stablecoins as a technology-neutral unit of value that “relies on a set of stabilization tools to minimize fluctuations of their price in such currencies”.

However, Lipton and other scholars disagree. To them, stablecoins are a technology-neutral payment system that is mutually exclusive with other forms of currency, and doesn’t require any interaction with the issuer.

Some important characteristics of stablecoins

Much of the ongoing debate on stablecoins revolves around how they are classified and used. Following Lipton’s definition, stablecoins can be organized into three groups: those that represent a legal claim (off-chain collateralized stablecoins), those that don’t but use their good faith (on-chain collateralized stablecoins), and those that don’t but rely on technology (uncollateralized stablecoins).

In the case of the first group, the issuer is held responsible if they fail to pay back. In claim-based systems, coin holders can redeem their coins using fiat money or commodities (such as gold), or reach out to a third party authorized to settle the claim.

Ensuring the stability of the second group is more complex. As there is no legal claim, the system’s strength depends on its own degree of accountability and openness. As a result, most stablecoin systems tend to avoid self-regulation and adhere to legal parameters. These are “good-faith stablecoins”, as they depend solely on the good business practices of the issuer.

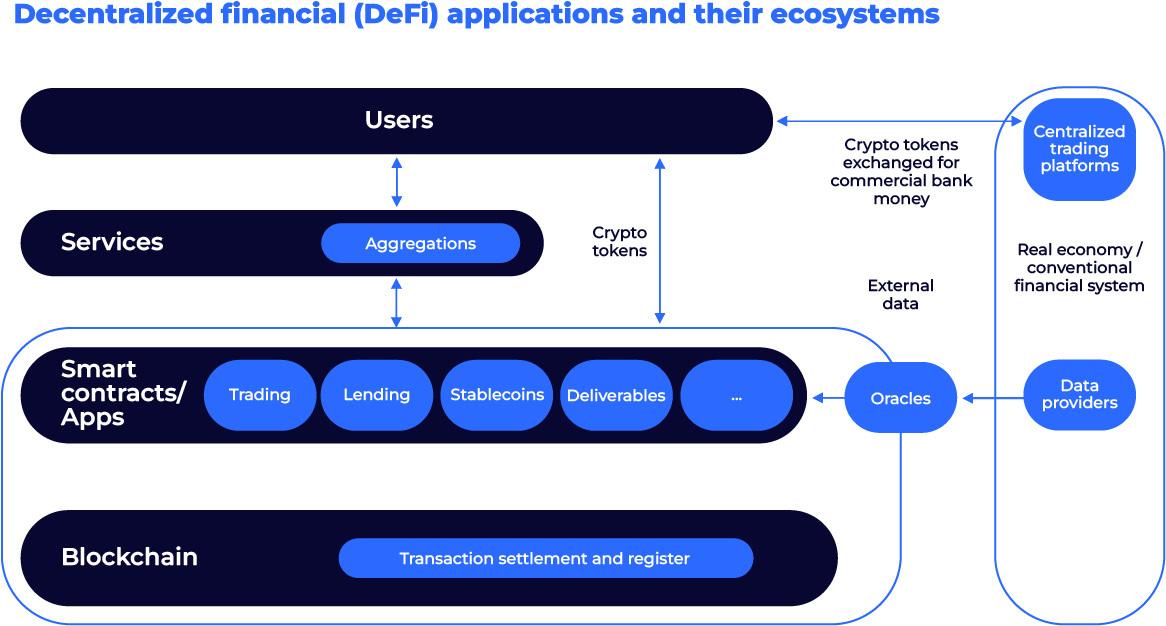

Diagram on how decentralized finance works, and how stablecoins fit into this process. Source: Deutsche Bank Research.

Good-faith stablecoins may rely on technology to manage crypto assets and encourage stable prices. The problem lies in using oracles — programs that provide external information into the blockchain.

From DeFi to global retail

Stablecoins are a trading tool for arbitrage opportunities in cross-border payments. They’re an instrument to convert volatile crypto into stable currency. Other use cases, such as receiving payment and remittances, are slowly gaining traction and becoming a solid payment alternative.

Out of all the examples we’ve just mentioned, none are as crucial as decentralized finance. According to a Deutsche Bank report, stablecoins are “commonly used for trading crypto assets on and between exchangers, offering fast and efficient transactions without requiring to convert their holdings into fiat currencies.

Using these as an exchange provides stability by depositing stablecoins into liquidity pools that provide funds for whatever purposes. This practice has gathered much traction very quickly. Deutsche Bank notes that in 2021 alone, collateral crypto assets grew from USD 30 billion to USD 234 billion.

Despite their generalized use in DeFi, stablecoins reached headlines until 2019, when Meta announced their plan to launch Libra. The main idea behind Libra (later on renamed Diem) was to create a stablecoin backed by a basket of different fiat currencies, allowing it to capture a large number of consumers. However, after receiving much criticism and resistance, Meta canceled the project.

Current concerns of stablecoins

As David Benko mentioned in a post about cryptocurrency, stablecoins (and cryptocurrency in general) carry operational reliability, safety, and robustness risks. Therefore, if we’re planning to scale stablecoins to a broader audience, major changes must be made to ensure efficient and safe transactions.

Experts also note that asset-backed stablecoins are reaching the size and scale of large money market funds (MMFs). According to FitchRatings, Tether’s actual holdings currently hold about USD 138 billion in collateral, which is roughly one-fifth of what the US prime MMFs now hold. Some stablecoin reserves are almost as large as some banks. This has sparked concerns over how this may affect regulated entities, financial stability, and the real economy.

Finally, there’s much discussion regarding transparency and regulation in stablecoins. We need legislation to protect the consumer, prevent abusive behavior, and fraud, and ensure the market adopts cryptocurrency without causing financial distress on a general level.

What the future holds for stablecoins

Stablecoins provide the stability most cryptocurrencies are currently lacking. Thus, they can cater to many industries and institutions currently interested in diving into distributed ledger technology (DLT)-based markets. It is important to note that most currencies using blockchain technology are still in their early stage. In other words, general use and implementation will require a collective effort.

This is an interesting idea to many, as many people visualize innovation as a disruptive event. However, innovation can also be a sustained process that involves many actors and processes. Considering stablecoin, sustained innovation is definitely necessary to ensure scalability and massive changes on a global level.

Was this article insightful? Then don’t forget to look at other blog posts and follow us on LinkedIn, Twitter, Facebook, and Instagram.

Author

Related posts