Legacy modernization and the future of fintech

December 9, 2021 -

10:04 pm

Nearly 80% of the world’s businesses run on COBOL, a first-generation programming language. With so many systems depending on ancient IT structures, how does the future of fintech and technology rely on legacy modernization?

This past spring, tens of millions of Americans waited weeks for their unemployment benefits. There were delays in 19 states, and all of them were attributed to issues with systems dating back almost 40 years or more

I know this sounds unbelievable, but it’s not the only case. In early 2019, the Costa Rican Social Security Fund, in charge of the country’s public health and insurance sector, announced they would be unable to make readjustments on salaries (such as bonuses) for at least 20 months. The reason? The system ran on COBOL and the only developers knowledgeable in that programming language were soon to retire.

Dealing with antiquated IT isn’t a struggle reserved for government institutions worldwide. Banking institutions, airlines, hospitals, and universities use legacy infrastructures.

In many cases, legacy systems are the backbone of any enterprise. They contain business-critical information that is difficult to modify or transfer.

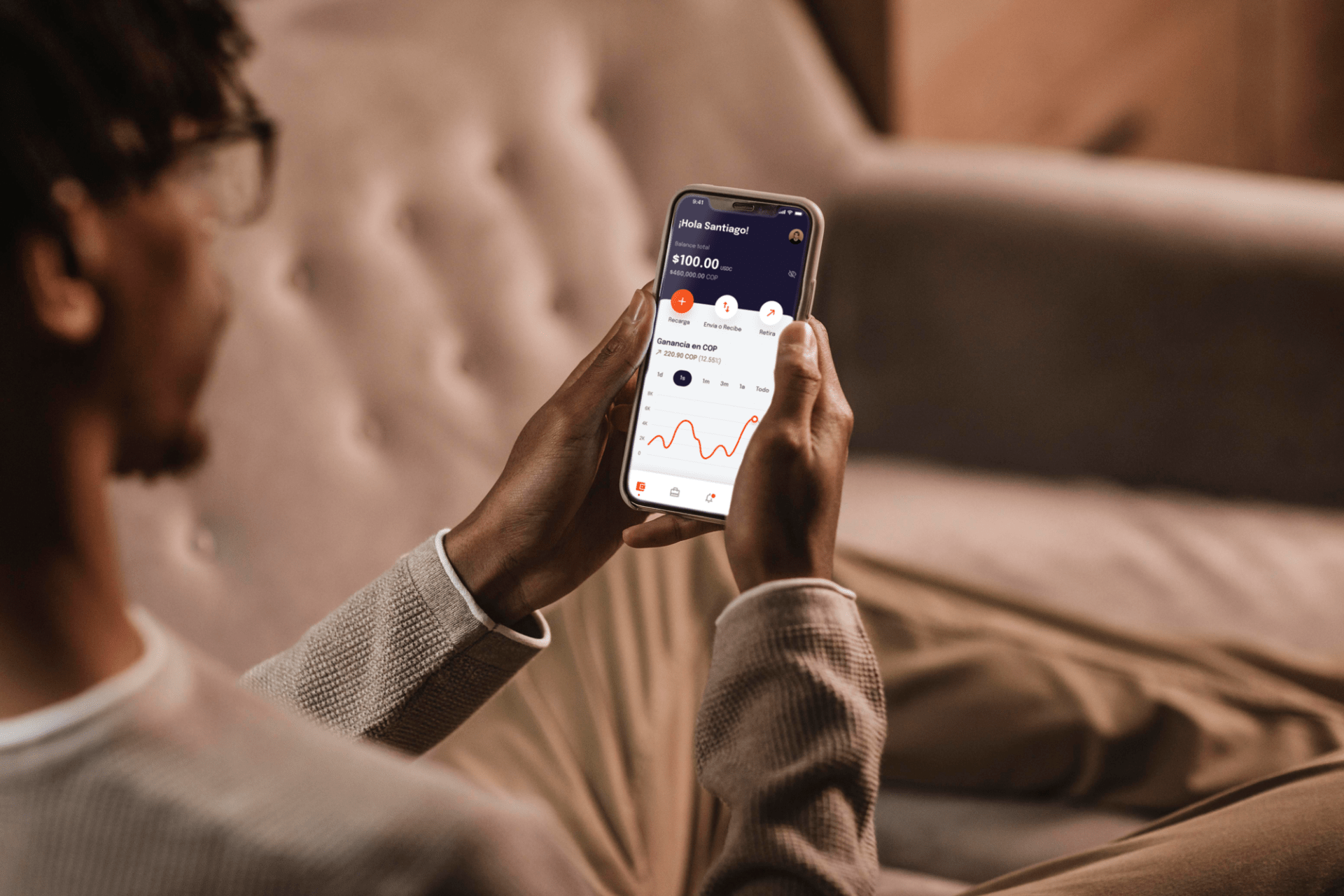

The fintech industry isn’t immune to the problems posed by legacy systems.

However, as technology progresses swiftly, banking and financial institutions face a problem: are legacy systems worth maintaining? Or does modernization justify the economic risk?

What’s legacy modernization?

There’s no formal definition for a legacy system. Known as an outdated critical system, it needs to be continuously maintained to satisfy changing user requirements. Nearly 80% of the world’s businesses run on COBOL, and more than half of the total IT costs result from legacy system maintenance.

Why is this so?

Companies put critical systems in place to respond to their primary objectives. However, when business needs deviate, most organizations turn to maintenance to keep the system operational.

Legacy systems can also evolve by re-developing, reusing, or migrating software components and platforms. According to the IEEE, organizations must cope with climbing operational and maintenance costs even with an evolving legacy system.

In the US alone, the government spent more than 80% of its 90 billion budget on the maintenance and operation of existing systems. Unfortunately, the maintenance budget is so elevated that it rarely leaves anything for modernization.

When maintenance fails, modernization is inevitable. Yet, this is not a simple process, either. And it can affect millions of customers if done incorrectly. For example, in 2018, the TSB Bank attempted to move its 1.3 billion records to a new banking platform. Because of the amount of data involved, migration turned out to be a bumpy process that affected website and mobile app access for over a week.

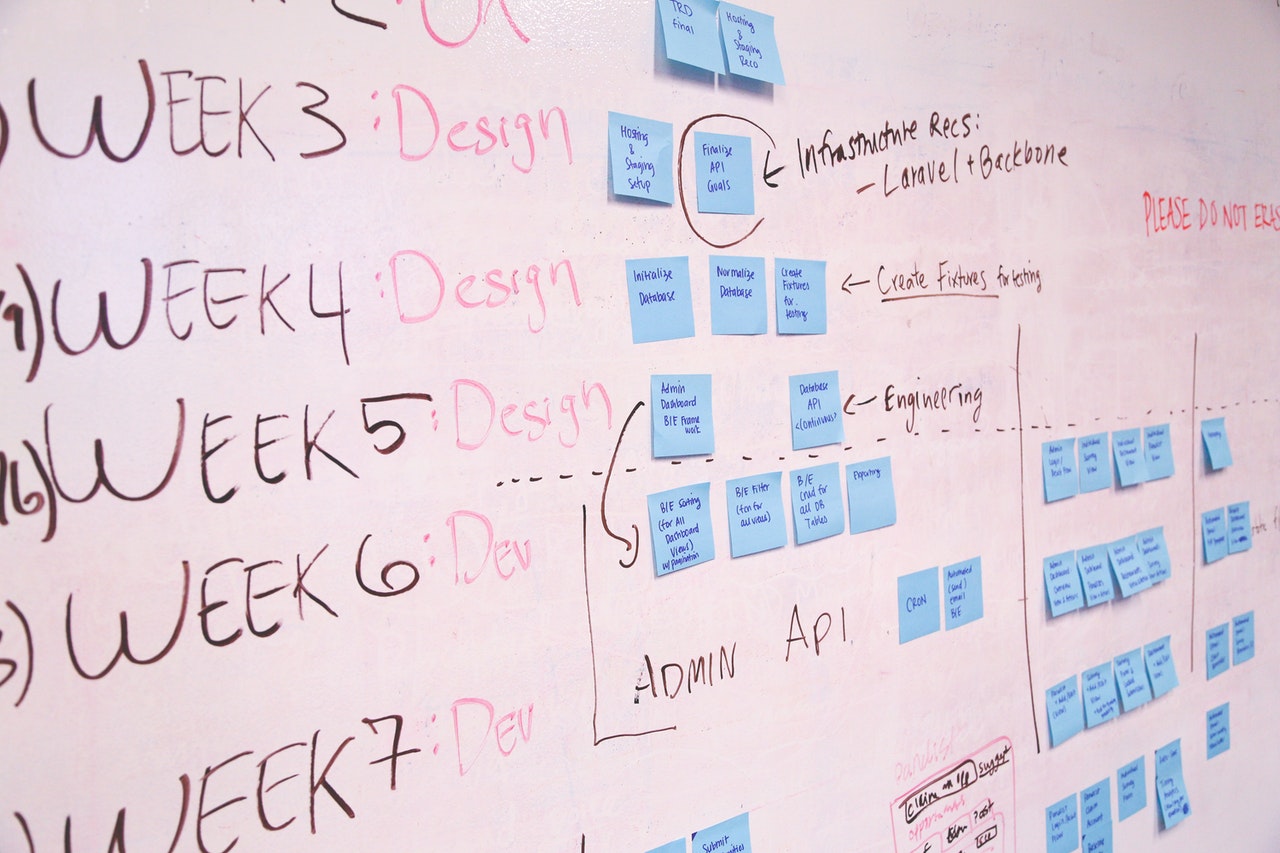

Where to begin?

Have you ever been in a situation where a problem needing solving is so massive you’re unsure how to begin? Legacy systems are like that. Thankfully, many methodologies can help leadership evaluate the risk-to-reward ratio of migrating a legacy system.

Gartner recommends a three-step evaluation to approach modernization. The first step is to understand the company’s drive towards change. Is the company not meeting new requirements? Or is the system compromising scalability, security, and compliance?

In the end, good opportunities for modernization come from having more than one reason or driving factor.

Once the key opportunities and problems are identified, the business must select the best modernization option. Implementations range from simple to most complex and are organized as follows:

- Encapsulating: Extending an application by encapsulating its data.

- Rehosting: Moving to a different infrastructure.

- Replatforming: Migrating to a new runtime platform.

- Refactoring: Restructuring code and removing everything that doesn’t work.

- Rearchitecting: Alter the code to shift to a new application.

- Rebuilding: Rewriting the application completely.

- Replacing: Changing the existing application for another.

The final step involves selecting the most appropriate modernization approach, that with the highest effect and value. Companies are responsible for mapping the seven modernization options in terms of technology, architecture, functionality, and cost.

Legacy modernization in fintech

Legacy systems are common in banking and finance, which shouldn’t be surprising. Core banking applications have been underinvested for years, which means many systems are not capable of supporting market expectations. The recent boom in fintech platforms has changed this, and many institutions are now starting to modernize.

However, a Deloitte report mentions that most banks are reluctant to modernize. Their reason? Legacy systems are so important to the overall banking architecture that any changes will have a widespread impact on the bank’s core platforms.

The need to implement new technologies into banking and financial services, along with the recent technology advances in application management make modernization more attractive. Migrating to cloud-native platforms or service-oriented platforms are viable options for banks, who now understand the short and long-term benefits of modernizing.

If your institution is aiming towards becoming a digital leader, the first step is to modernize your legacy system. As the gap between success in online applications and the status quo grows wider day by day, evaluating the costs, risks, and challenges of modernization is now a required discussion among team leaders and decision-makers.

So, are you ready to modernize?

Was this article insightful? Then, don’t forget to look at other blog posts and follow us on LinkedIn, Twitter, Facebook, and Instagram.

Author

Related posts